A Long-Term Incentive Plan, commonly known as an LTIP (and often casually referred to as an ESOS), is an incentive structure where a company rewards selected employees, directors, or key management personnel (“Employees”) with free shares or share options over a period of time.

The Employees will only enjoy such benefits after meeting certain conditions, such as remaining with the company for a fixed period, achieving performance targets (KPIs), or helping the company reach specific business milestones.

The LTIP may also be structured to apply not only to the Employees of the company itself, but also to the Employees of its subsidiary companies. This is particularly useful for a group structure where the parent company wishes to reward and retain key talents across different subsidiaries under the same group.

An LTIP is commonly used to:

There are a few common structures, but the two main structures are Share Grant and Share Option.

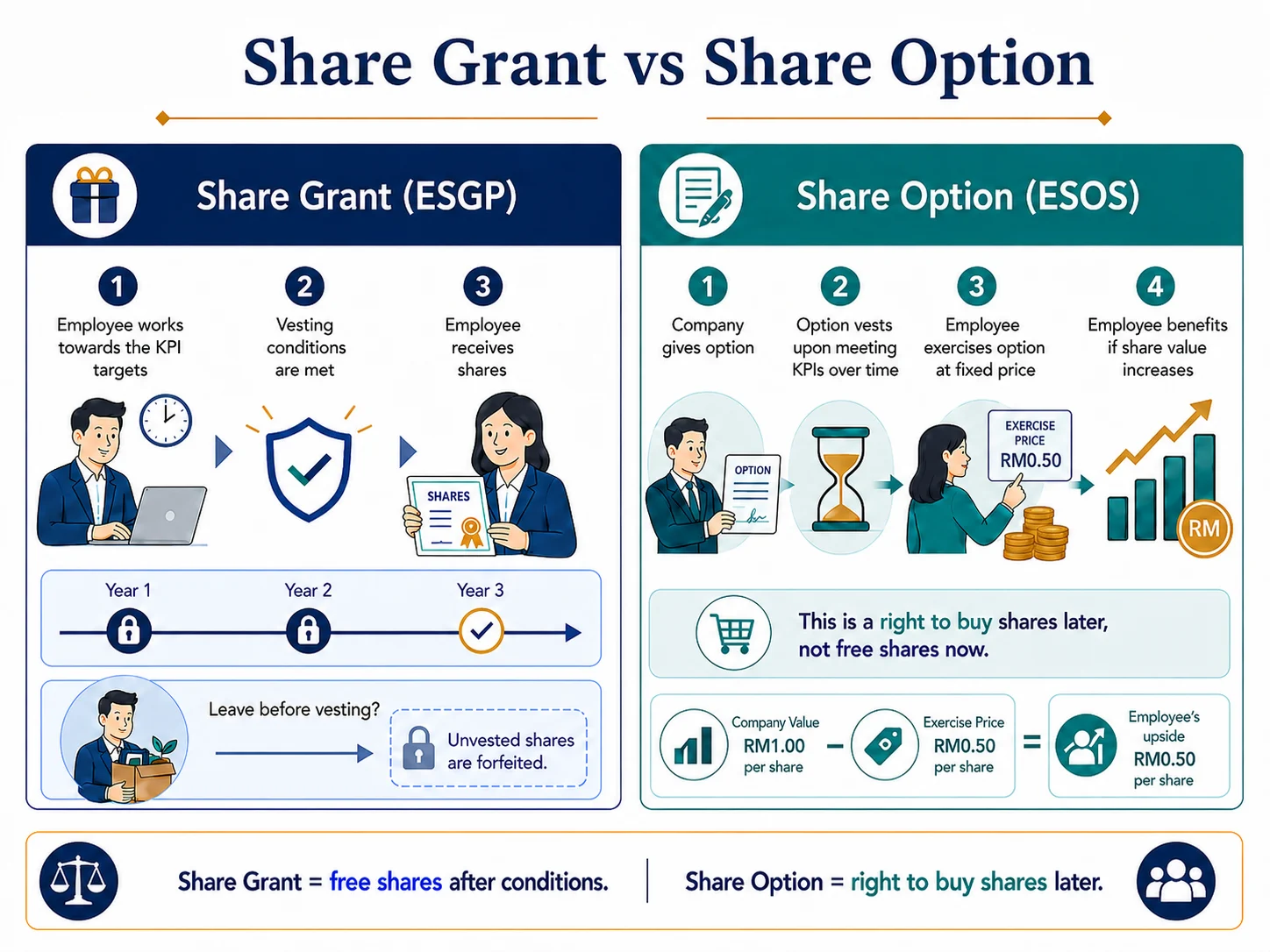

Under a Share Grant structure, the company grants shares to the Employee after the Employee satisfies the vesting conditions.

For example, the company may grant 10,000 shares to a key Employee, but the shares will only vest over a period of 3 years. If the Employee resigns before the vesting date, the unvested shares will be forfeited.

This structure is commonly understood as giving “free shares” to the Employee, but the Employee will only enjoy the shares after fulfilling the required conditions.

Under a Share Option structure, the company gives the Employee the right to subscribe for shares in the future at a fixed price.

For example, the Employee may be given an option to subscribe for 10,000 shares at RM0.50 per share. If the company grows and the value of the shares increases, the Employee benefits from the increase in value by exercising the option at the agreed price.

This structure is commonly understood as giving the Employee a “right to buy shares”, rather than giving free shares immediately.

To implement an LTIP properly, the company should prepare the following documents:

The By-Laws are the main rulebook of the LTIP. They set out the rights, obligations, conditions and procedures of the scheme.

They typically cover:

These documents are used for actual implementation.

The company’s Constitution should be lodged, reviewed and, if necessary, amended to support the implementation of the LTIP.

This is important because once an Employee becomes a shareholder of the company, the Employee will generally be bound by the company’s Constitution in his or her capacity as a shareholder. Therefore, the Constitution should contain clear provisions to regulate the rights, restrictions and obligations of employee shareholders

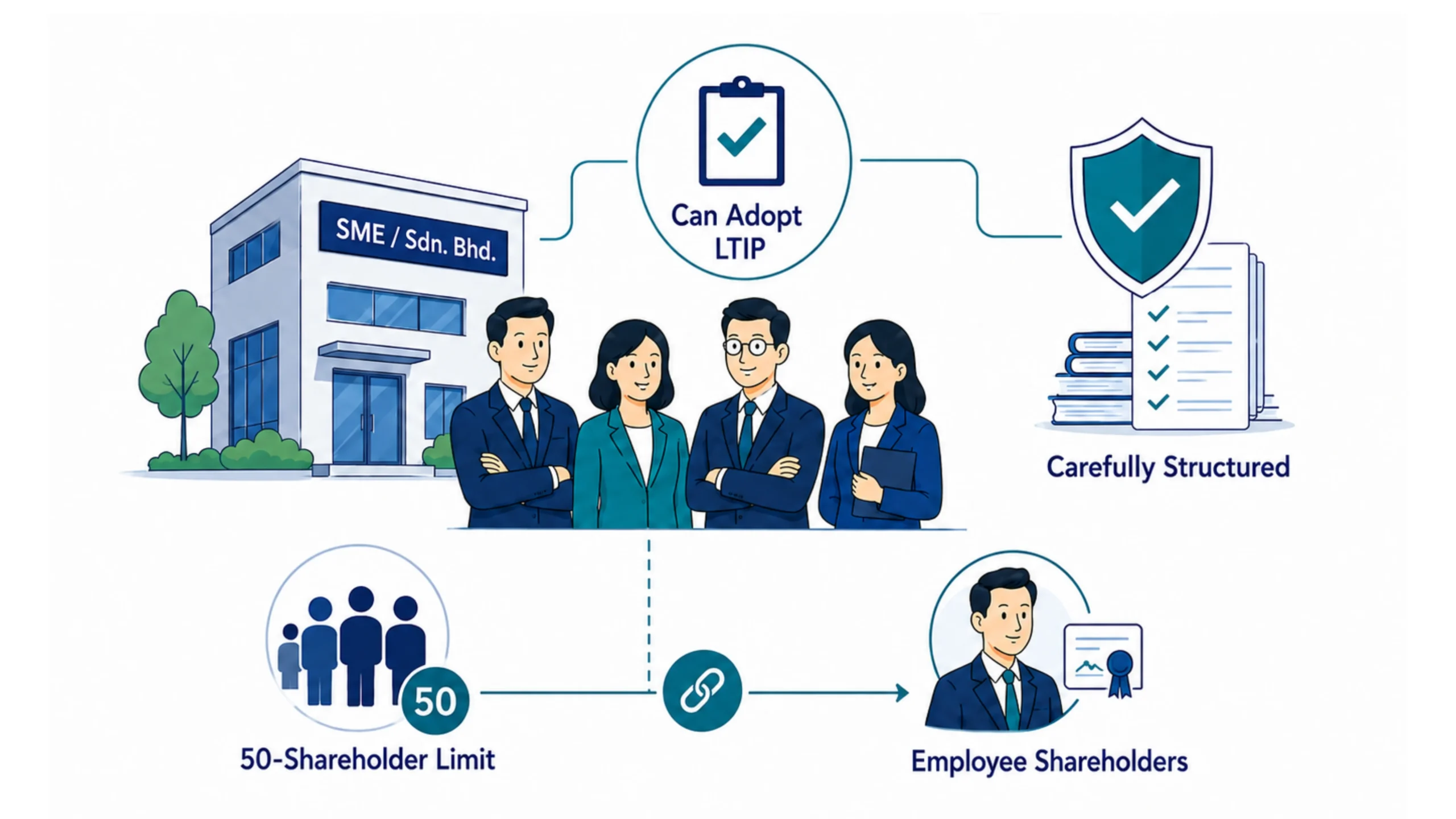

Yes, an SME or Sdn. Bhd. can adopt an LTIP.

LTIPs are commonly seen in Berhad companies, especially public listed companies, because they usually have a larger management team, clearer share value, and may be subject to formal shareholder approval, Bursa requirements and disclosure obligations.

However, the concept of an LTIP is not limited to Berhad companies. It may also be adopted by SMEs, provided that the structure is carefully designed. This is because an SME is usually incorporated as a private company (Sdn. Bhd.), and is subject to the 50-shareholder limit applicable to private companies under Section 42(1) of the Companies Act 2016.

That said, Section 42(3)(b) further provides that, in determining the number of shareholders in a private company:

“a shareholder who is or was an employee of the company or its subsidiary when they became a shareholder shall not be counted.”

This means that employee shareholders are not counted towards the 50-shareholder limit, provided they became shareholders while they were employees of the company or its subsidiary.

In practice, although the law provides this exclusion, the company should still structure the LTIP in a clean and well-documented manner. This is to avoid the arrangement being misunderstood as a public offer of shares, an uncontrolled expansion of shareholders, or a scheme that is inconsistent with the nature of a private company.

LTIPs are commonly used as part of a formal employee incentive structure. For SMEs and Sdn. Bhd. companies, the same concept can also be adopted, provided that the structure is carefully designed to suit the company’s shareholding structure and future business plans.

However, an LTIP should be properly structured from the beginning. The company should be clear on the type of award, eligibility criteria, vesting conditions, leaver provisions, transfer restrictions and the rights attached to the shares or options. The company should also consider the relevant tax and accounting treatment before implementing the LTIP.

When structured properly, an LTIP is not merely about giving shares. It becomes a structured framework to reward the right people, retain key talents, and support the sustainable growth of the company.

Disclaimer: This article is for general information purposes only and does not constitute legal advice. Specific advice should be sought based on the facts and structure of each transaction.